Although traditional finance products have slowly made their way onto web3 platforms, credit risk infrastructure remains largely off-chain. Up until now.

Spectral a web3 startup, has developed a credit risk assessment infrastructure that enables on-chain credit scores for decentralized finance (DeFi) decisions. Spectral’s platform fulfils a need for trustless, permissionless credit analysis so Samsung Next invested in it.

Samsung Next joined a $23 million Series B round led by General Catalyst and Social Capital. Other investors include Circle Ventures, Franklin Templeton, Gradient Ventures, Jump Capital, and Section 32.

The Spectral team is led by CEO Sishir Varghese, an experienced blockchain entrepreneur. His two co-founders, Kevin Choi and Sirkar Varadaraj, are blockchain visionaries who studied computer science at New York University.

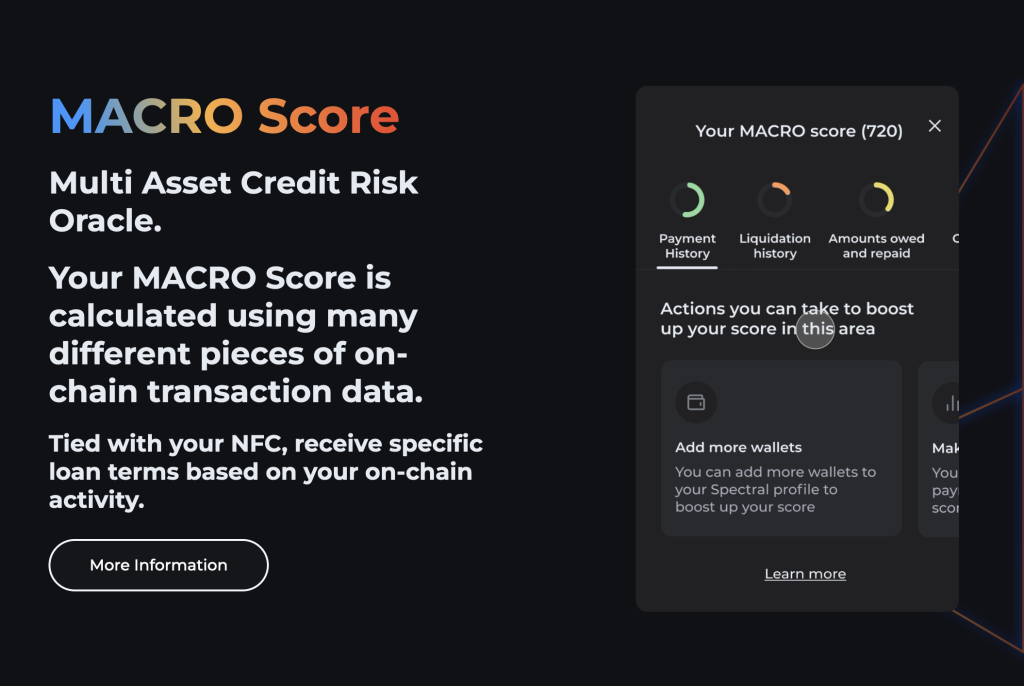

The Multi-Asset Credit Risk Oracle (MACRO) score developed by Spectral enables lenders and consumers to check creditworthiness via a new primitive built for the pseudonymous economy. MACRO scores, which are comparable to the now-ubiquitous FICO scores, are calculated using on-chain transaction data tied to DeFi lending and borrowing activities, as well as general on-chain history. By disintermediating existing legacy institutions, and adding transparency to the calculation of credit scores, Spectral enables consumer lending decisions to leverage on-chain data.

A DeFi solution for credit risk assessment has important implications for financial institutions. While web3 smart contracts and loan decisions can be made almost instantaneously, DeFi loans are often over-collateralized to compensate for the lack of a reliable tool for assessing credit risk on-chain. The ability to assess credit risk is essential for DeFi, in which financial institutions rely on inherently trustless, open source applications to make lending decisions.

Spectral enables lenders to harness the transparency of blockchain data in order to evaluate the creditworthiness of a borrower. Moreover, instead of a cumbersome process for evaluating risk, lenders can rely on MACRO scores that are calculated using on-chain transaction data that includes payment history, liquidation history, debt, repayment history, assets, credit utilization, and other factors impacting creditworthiness.

Verifiable computation and zero-knowledge proofs, published alongside MACRO scores, will enhance transparency on the Spectral platform, and will give lenders confidence in each risk assessment. Distributed credit risk modeling also will enable credit scores developed by different entities to be aggregated to provide a more robust and holistic view of a borrower’s history and risk.

Spectral also wants to make it easy for users to bundle together their Ethereum wallet addresses to provide the data needed for holistic credit risk assessment. This bundling, called Non-Fungible Credit (NFC), enables consumers to sync their on-chain transactional history into a single composable asset (ERC-721). The combination of MACRO scores and NFCs represents a new asset class of programmable creditworthiness.

We think Spectral’s platform will help accelerate the growth of DeFi lending. Democratized and decentralized credit risk assessments will lead to a more capital-efficient credit landscape in which trust reigns supreme in a trustless ecosystem that no longer requires third party intermediaries.