Sit down and grab a drink because this is going to be a long ride!

Starting from the basics, Nexo allows any user to buy, sell, or swap four different types of coins/tokens.

- Crypto Currencies (e.g., BTC and ETC)

- Fiat Currencies (e.g., EUR and US dollars)

- Stable coins (e.g., USDT and USDC)

- Nexo Tokens

The first one represents digital currencies. The second one represents government-issued currencies. The third one represents digital currencies that are linked to a fiat currency. And the last one represents the tokens of the company and they give us access to the different features of the Nexo platform.

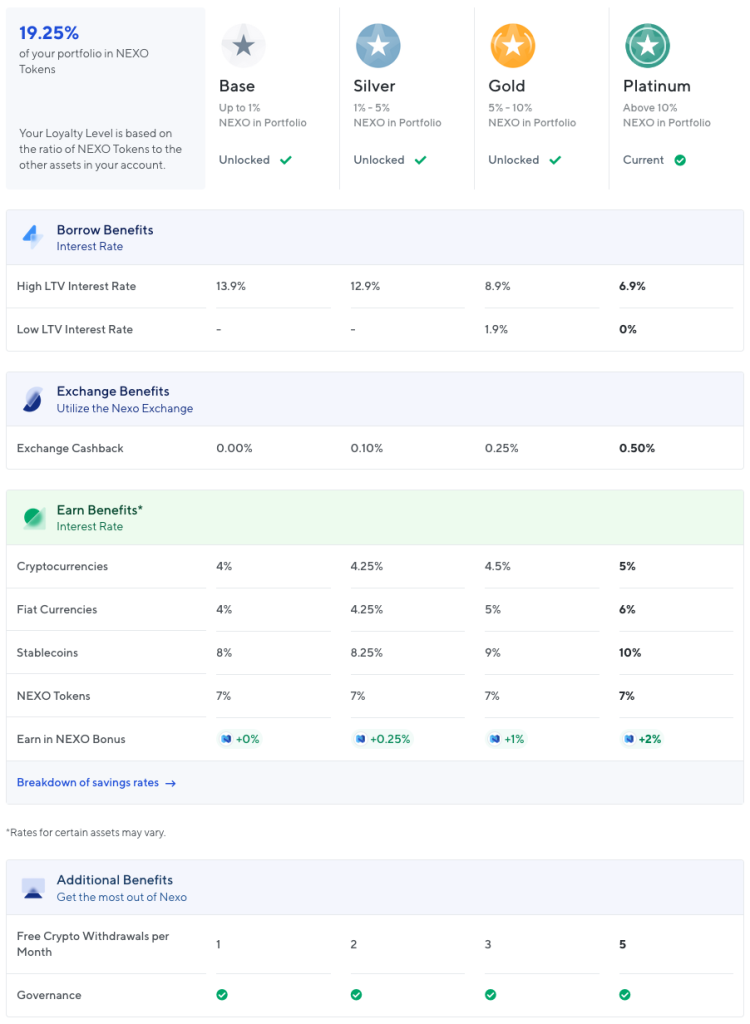

Now, with that in mind, Nexo divides all users into different loyalty levels depending on how many Nexo tokens they have compared to the total amount of coins/tokens in their portfolio (sum of all four coins/tokens mentioned above). For example, if someone has 5000 USDT and 100 dollars in Nexo tokens in their portfolio, their Nexo tokens represent 19.6% (100/5100) of their portfolio, and hence they will be in the Platinum level. You can check the Loyalty levels and their benefits here –

Considering that, depending on the coins you are holding in your portfolio and your loyalty level, it may happen that you can borrow money at an APY lower than the APY you are receiving from your coins, and thus earn some extra passive income.

For that, we need to understand the following concepts.

First, we have the Loan-To-Value, which represents how much is the loan compared to the value of the assets securing the loan. More specifically, before you get a loan, you need to keep in mind that you will have put some money away into collateral, meaning that you will have to put away some money to secure so that you will be able to re-pay your loan.

Now, on Nexo, the money that is in collateral does not earn interest and the money not used for collateral receives interest. To distinguish between these two, Nexo refers to them as Credit Line Wallet (collateral assets) and Savings Wallet.

Putting it all together, if we have for example 1000 USDT in our portfolio and we put it all into collateral and borrow 100 USDT, the LTV is 10% (100/1000). But, if we continue with that example, you will not earn any interest because everything is in the Credit Line Wallet and you will have to pay for borrowing money.

Now, since the maximum LTV for USDT is 90% (you can check the maximum LTV for each type of coin/token here), we can play around and take some money out of the Credit Line Wallet and put it into the Saving Wallet. For example, if we leave 200 USDT in the Credit Line Wallet and transfer 800 USDT to the Savings Wallet, then the LTV would be 50% (100/200) and you will earn interest from 800 USDT.

If that is clear, the next thing to ask ourselves is why this LTV is so important? Well, if you are in the Platinum level and your LTV is less than 20%, you can borrow money at 0% APY. Otherwise, if you are in the Platinum level and your LTV is more than 20%, you can borrow money at 6.9% APY.

Similarly, if you are in the Gold level and your LTV is less than 20%, you can borrow money at 1.9% APY. Otherwise, if you are in the Gold level and your LTV is more than 20%, you can borrow money at 8.9% APY.

How does it all play together?

Let’s take for example that your portfolio has 100 dollars in Nexo tokens and 900 USDT, and you want to borrow 400 USDT. Your Loyalty level before getting the loan is Platinum level because your Nexo tokens represent 10% of your portfolio [100/(100+900)], but your loyalty level after getting the loan would be Gold level because your Nexo Tokens represent 7.1% of your portfolio [100/(100+900+400)]. Then, you put 500 USDT into collateral, such that your LTV becomes 80% (400/500).

Let’s say you want to receive the interest in the same currency as your coins/tokens. In that case, and given that you are now in the Gold level, you will receive 7% APY interest for your 100 dollars in Nexo Tokens, and 9% APY interest for your 400 USDT in the Savings Wallet, and pay 8.9% APY for your borrowed 400 USDT.

So, the strategy comes down to playing with the money in your portfolio, your loyalty level, and the money in the Credit Line/Savings Wallets.

Via this site